Kevin Warsh, former governor of the US Federal Reserve, speaks with CNBC on July 17, 2025.

CNBC

Kevin Warsh could face a buzzsaw when he takes over as Federal Reserve chair — a Hobson’s choice between fighting inflation and protecting the labor market.

The Fed is duty-bound to support both sides of its sometimes conflicting dual mandate: stable prices and full employment.

There essentially are three ways to do that: raise interest rates to fight inflation by dampening demand, lower rates to support economic growth and hiring, or — most preferably — keep rates where they are to maintain a balance between the two.

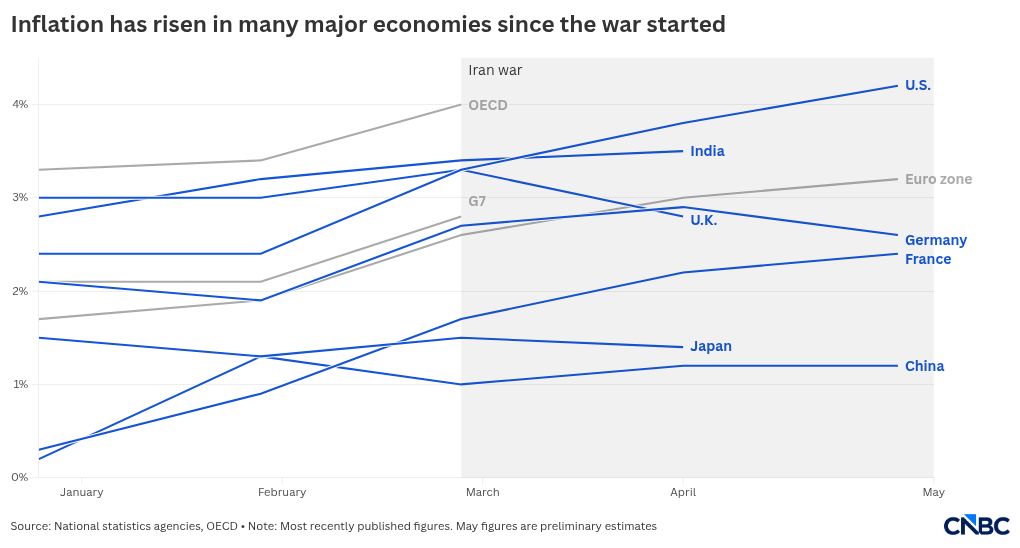

Brewing economic conditions suggest, however, that when Warsh takes office, presumably in May, central bank policymakers could be facing both a wobbly jobs picture and sticky inflation made worse by spiraling energy prices.

“He’s got a perfect storm awaiting him here,” said Troy Ludtka, senior U.S. economist at SMBC Nikko Securities. “We’ve got some significant stagflationary pressures, particularly from the manufacturing and goods sectors of the economy. This is coming at a time when it seems like we’re really beginning to see the consumer — I don’t want to say break — but maybe begin to break.”

Stagflation, or high inflation and low growth, is a Fed official’s worst nightmare. It can mean having to prioritize one side of the mandate over the other, and in turn risk losing both.

In the current environment, the Iraq war has pushed up energy prices sharply, with U.S. crude oil briefly soaring over $100 a barrel on Monday before slipping backwards after President Donald Trump provided assurance that the conflict will be over soon.

For Warsh, though, the stakes are particularly high.

Tough choices

Trump has made no secret that he expects Warsh to push for substantially lower interest rates. The president and other administration officials have been contending — at least before the war began — that inflation is no longer a significant threat to the economy and that the Fed should continue the rate cuts it began last September.

Pleasing the president might not be so easy.

Even before the energy surge, manufacturing costs had been rising. An Institute for Supply Management price gauge hit a nearly four-year high in February, with purchasing managers at U.S. factories reporting continued cost increases, fed in part by Trump’s tariffs.

Ludtka warned that if energy prices remain elevated, headline inflation could climb over 3% even as consumer finances look pressured and the labor market is softening.

Economists generally assign low pass-through effects from higher energy prices to the broader economy. However, since the fighting began, the price of urea fertilizer has soared 15%. Higher fertilizer costs often translate into rising food prices, raising the possibility of renewed inflation pressures ahead.

For his part, Warsh faces a Federal Open Market Committee already divided over the future path of policy. While central bankers usually look through oil shocks as drivers of longer-term economic trends, they may have little choice but to address longer-term disruptions.

Rate cuts still possible

“He’s running into an environment where the committee is extremely divided. That division is only going to increase from here,” Ludtka said. “If oil prices remain high, and inflation is likely to remain well-supported in the face of a weak labor market, it’s going to force them to move to one side or the other.”

Despite the threat of higher inflation, Ludtka added he believes “the path of least resistance for policymakers is lower rates.”

One thing the Fed — and Warsh as incoming chair — has in its favor is a consumer who continues to spend, though the strength is concentrated among higher-income households.

Consumer spending rose 3.2% in February from a year earlier, the biggest increase in more than three years, according to Bank of America data. The firm noted, however, that after-tax wage growth for top earners rose 4.2% annually compared with just 0.6% for lower earners — the widest gap in the data series going back to 2015.

Monetary policy has proven to be an ineffective weapon against inequality.

Still, Fed officials might be more tempted to look through a temporary oil spike if further signs emerge that consumers — particularly among these at the lower end of the income spectrum — are struggling with both higher prices and a weakening labor market.

Bank of America economists also believe the market may be misreading the current situation by anticipating that the Fed automatically will prioritize inflation. Traders have pulled back expectations in recent days for rate cuts, expecting the first move not to come until September and taking a second one off the table until 2027.

“The market response to the oil price spike has been mostly hawkish,” BofA economist Aditya Bhave said in a note. A hawkish Fed is more apt to focus on inflation and keep rates higher. “This could be a mistake.”